Staff Reporter | Duranta TV | Agartala

A fresh controversy over financial discipline, accountability, and public fund management in the Tripura Government has emerged following the Comptroller and Auditor General (CAG) Audit Report for the financial year 2023–24.

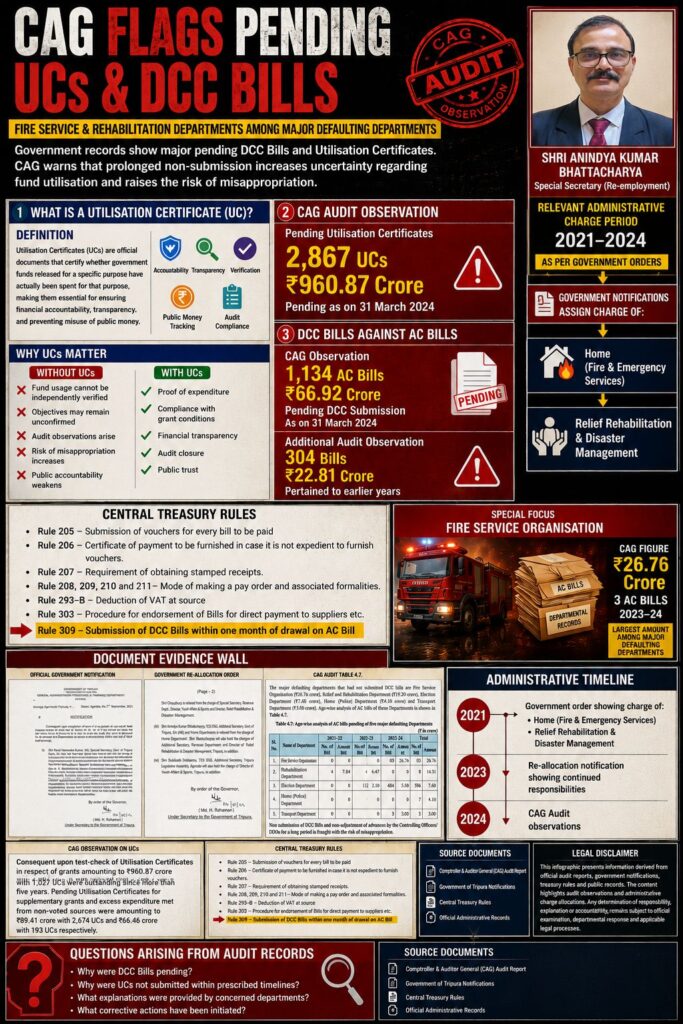

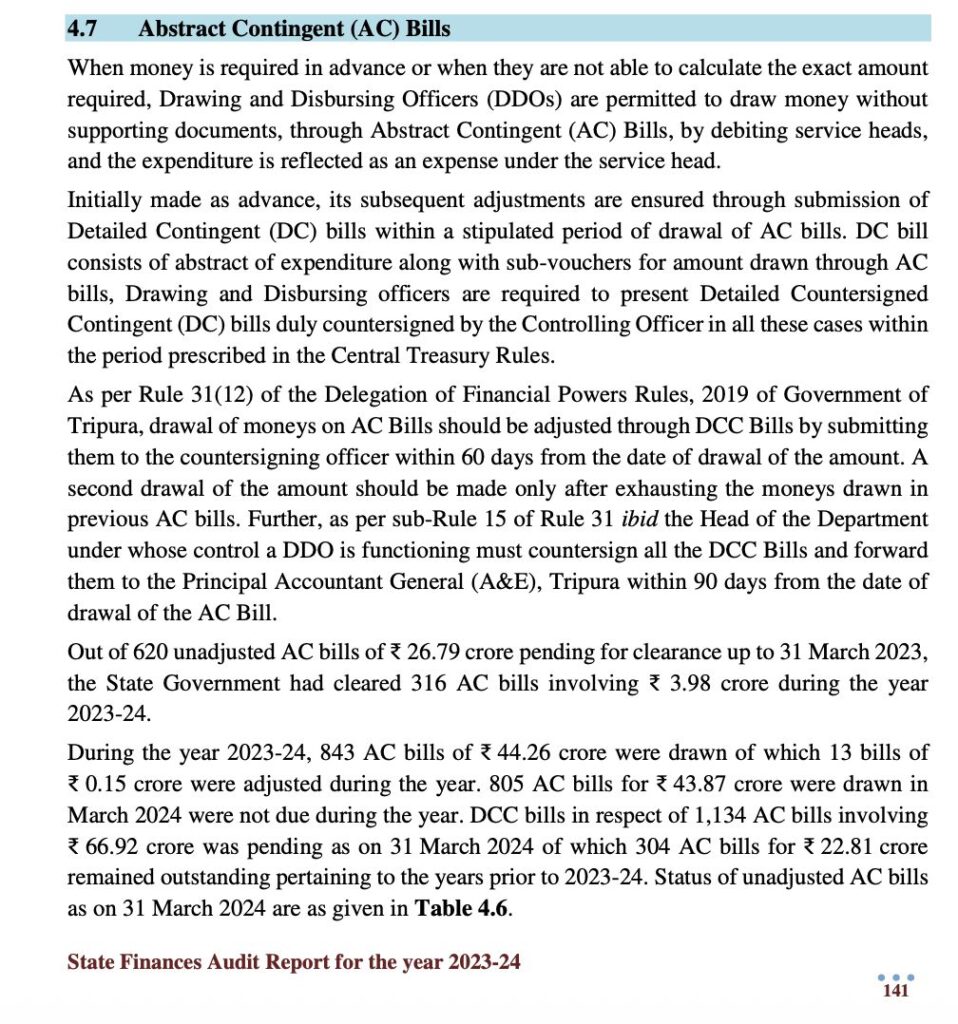

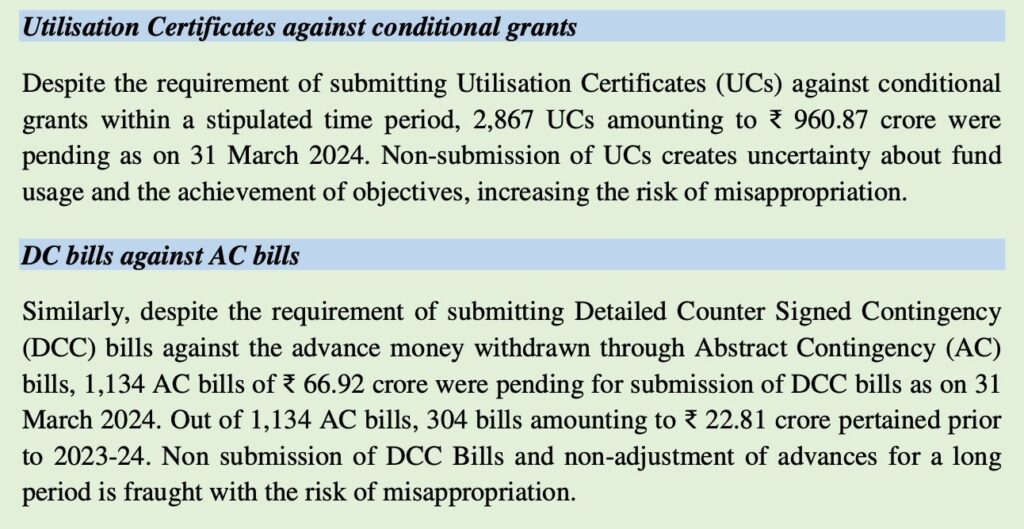

According to the report, as of 31 March 2024, a total of 1,134 Abstract Contingency (AC) Bills involving ₹66.92 crore remained unsettled because the mandatory Detailed Countersigned Contingency (DCC) Bills had not been submitted. As a result, a huge amount of public money has remained unadjusted for years.

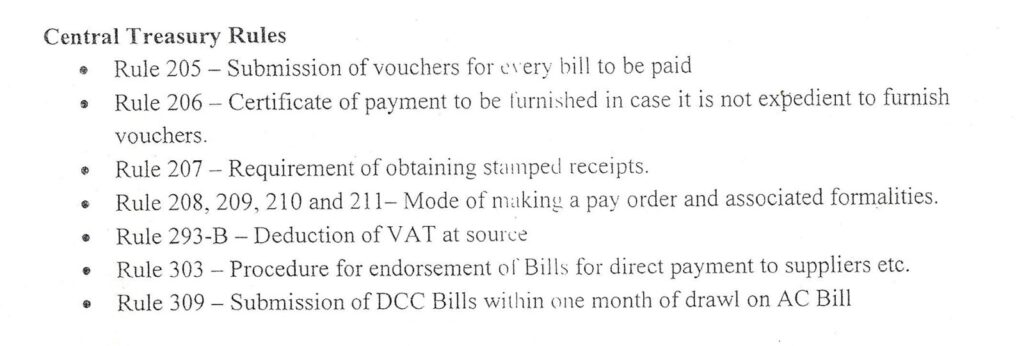

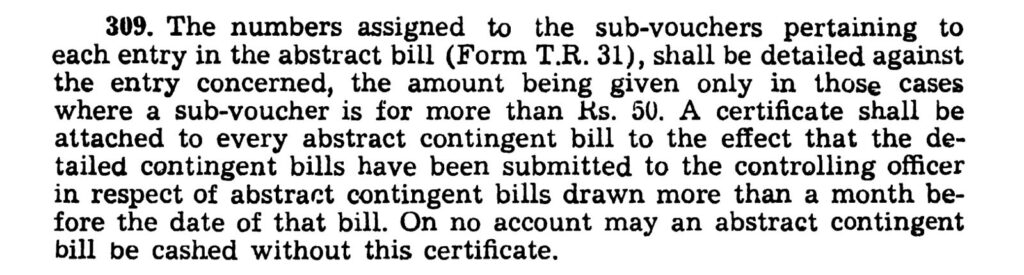

Under Rule 309 of the Central Treasury Rules and Rule 31(12)(v) of the Delegation of Financial Powers Rules, 2019, advance money withdrawn through AC Bills must be adjusted within a specified period by submitting DCC Bills. Rule 309 requires submission within one month, while DFPR provides a maximum period of 60 days for adjustment.

However, the CAG’s observations present a completely different picture.

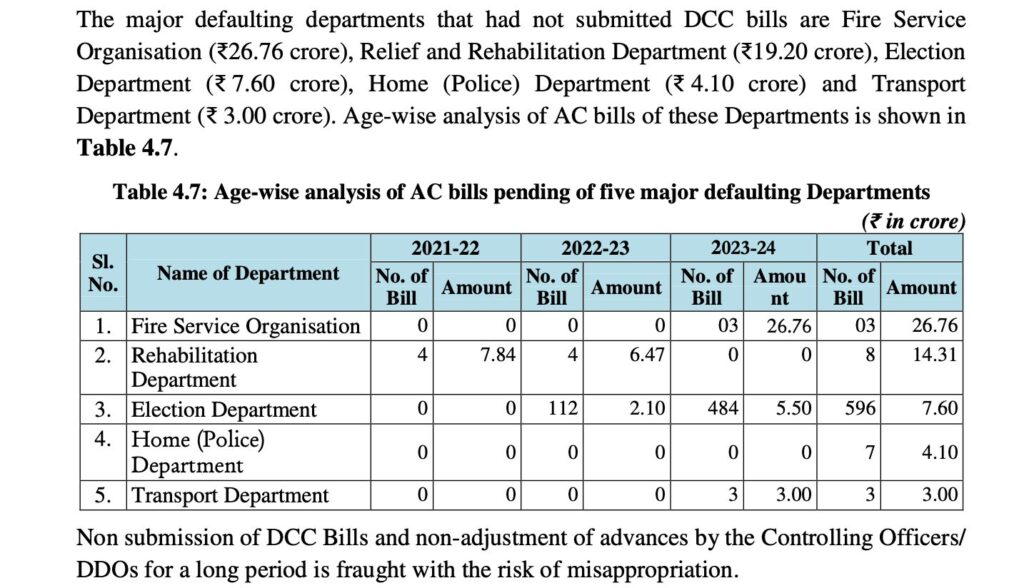

The audit found that out of the 1,134 unsettled bills, 304 bills worth ₹22.81 crore relate to periods before the financial year 2023–24. In some cases, bills have remained unadjusted since 2021.

Even more concerning is the fact that the CAG has clearly warned that failure to adjust AC Bills and submit DCC Bills for long periods creates a risk of misappropriation of funds. In other words, the CAG has indirectly pointed towards the possibility of misuse of public money.

This raises an important question: if money is withdrawn from the government treasury and its detailed expenditure accounts are not submitted for years, what were the officials responsible for ensuring compliance with financial rules doing?

According to the audit report, the highest amount of unsettled bills was found in the Fire Service Organisation (₹26.76 crore) and the Relief & Rehabilitation Department (₹19.20 crore).

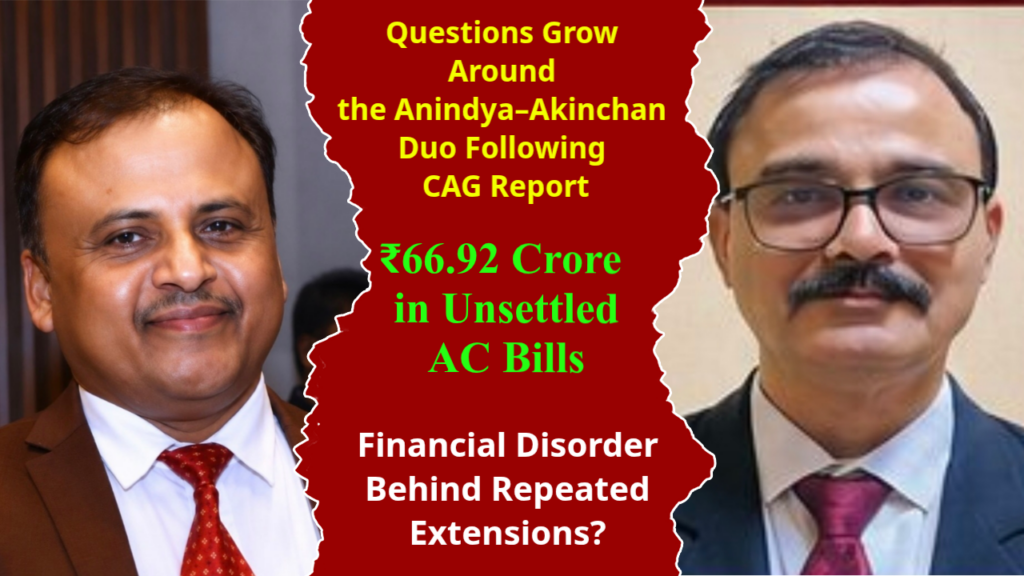

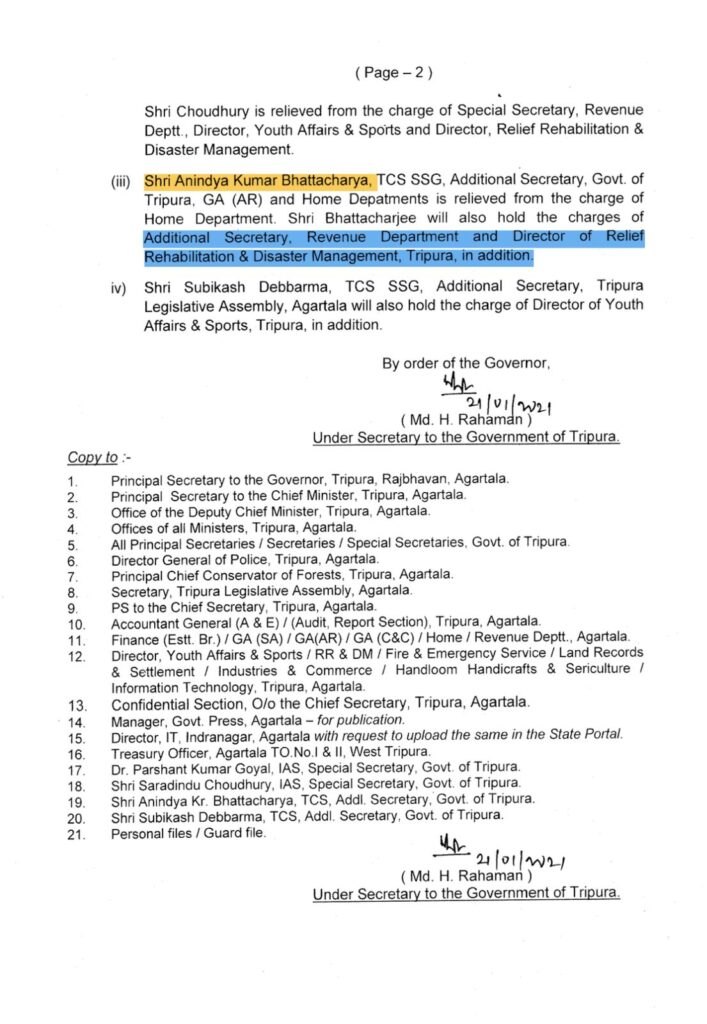

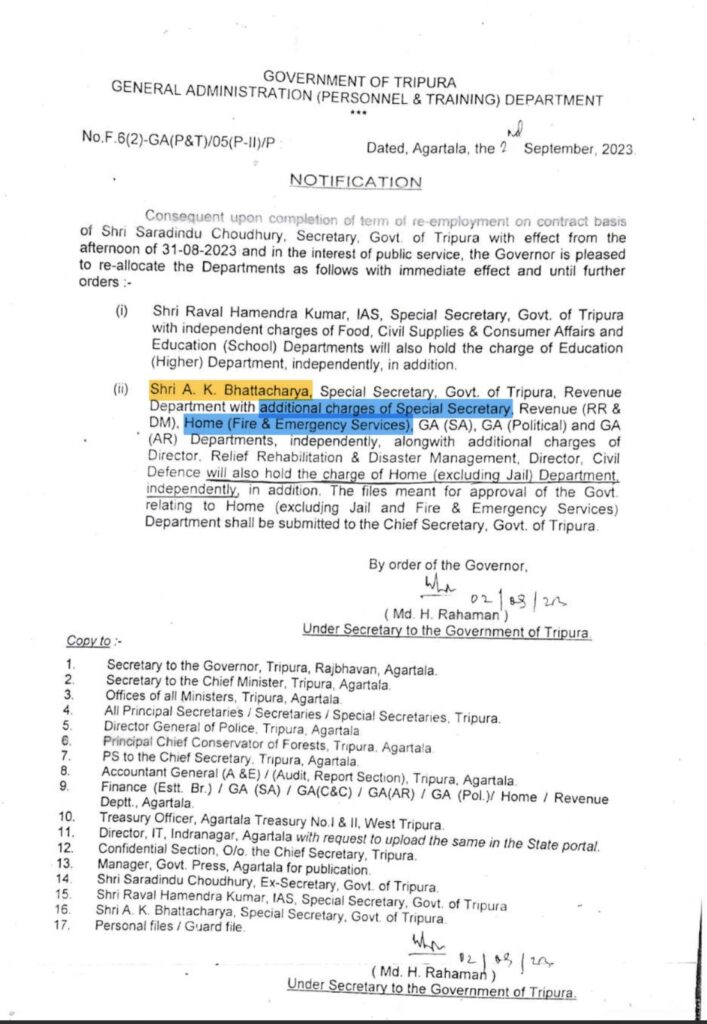

In both these cases, discussions within administrative circles have brought attention to former IAS officer Anindya Kumar Bhattacharjee. According to official records, he held responsibility for several important departments at different times, including Revenue, Relief Rehabilitation & Disaster Management, and Home Department (Fire & Emergency Services). Not only that, even after retirement, he has received seven extensions and continues to hold an important position in the Secretariat.

Official notifications show that additional responsibilities related to Revenue and Relief Rehabilitation & Disaster Management were also entrusted to him. Therefore, questions are now being raised about the effectiveness of financial supervision and administrative monitoring during the period concerned.

Meanwhile, during the financial year 2023–24, while serving as Special Secretary in the Fire Service Organisation, the department reportedly received excess and unnecessary grants amounting to ₹493.93 lakh, including ₹100 lakh received through a Supplementary Grant, as mentioned in audit documents.

On the other hand, Akinchan Sarkar has been serving in an important position in the Finance Department for a long time. Questions are now being raised within the Secretariat regarding how active the Finance Department was in addressing the continued pendency of AC Bills, non-submission of Utilisation Certificates, and weaknesses in financial accountability.

There is growing discussion within sections of the Secretariat that during the administrative tenure of Anindya Kumar Bhattacharjee and Akinchan Sarkar, these financial irregularities and monitoring failures were allowed to continue for years. However, no final government investigation report has yet been published to establish such allegations.

Nevertheless, several fundamental questions remain unanswered.

Were all AC Bills regularly monitored?

Were DDOs instructed to submit DCC Bills within the prescribed time limit?

Was any action taken against officials who defaulted?

If reminder notices were issued, where are the compliance reports?

Were departmental reviews actually conducted?

Has any departmental inquiry been initiated to fix responsibility?

And most importantly, why has the Finance Department remained silent for so long?

1,134 AC Bills Unsettled, ₹66.92 Crore Unaccounted For: Under Whose Watch Did This Failure Continue?

CAG Warning: Unsettled Bills, Unanswered Questions from the Finance Department, Administration Under Scrutiny

Where Is the Account of Public Money? Fresh Controversy Around the Anindya–Akinchan Chapter

The CAG report also states that thousands of Utilisation Certificates involving hundreds of crores of rupees are still pending. This points towards deeper structural weaknesses in financial reporting and public financial management.

₹66.92 crore is not a minor accounting error. It is taxpayers’ money. The failure to submit detailed expenditure accounts within the prescribed period naturally raises questions about accountability and transparency.

More questions arise. If Rule 309 makes it mandatory to submit DCC Bills within one month, how did hundreds of bills remain unsettled for years? Why were the advances not adjusted? Were explanations sought from the responsible officials? If not, why not?

Does this not go against the principles of Good Governance, Ethical Governance, Fiscal Prudence, and Fiscal Discipline?

Most importantly, when the country’s highest audit institution, the CAG, itself warns about the risk of misappropriation, what steps has the government taken to assure taxpayers that every rupee has been properly accounted for?

According to administrative observers, the answers to these questions will determine whether this is merely a case of administrative negligence or evidence of a deeper crisis in financial governance.

The issue of repeated re-employment of retired officials has also become controversial. Questions are being raised in various quarters regarding the government’s position on Anindya Kumar Bhattacharjee, who has received seven extensions after retirement and continues in office.

Some have even begun comparing the practice of reappointing retired officials with controversial administrative decisions seen in other states.

Attention is now focused on one key question: Following these serious observations by the CAG, will the government initiate an impartial investigation, fix accountability, and restore financial discipline, or will it continue to retain the concerned officials in their positions without taking any action?

To be Continue…